Angela Hunter is a standout leader in the insurance and tech industries, known for her innovative approach. She started her career at PwC but quickly shifted her focus from accounting to management and marketing. After six years, she moved to Vodafone, where she successfully launched a new segment in prepaid mobile technology, handling the challenges of a startup environment with ease.

Her success caught the eye of NRMA Insurance Australia, where she led major initiatives for eight years, including direct commercial insurance and remote home security systems. Angela then made significant contributions at Citibank, GE Capital, and Chubb, achieving 56% growth over five years by focusing on the millennial family market. She later joined Prudential in Singapore, continuing to make a strong impact in the industry.

Angela’s expertise then led her to Citibank, GE Capital, and Chubb, where she achieved an impressive 56% growth over five years by targeting the millennial family segment. Later, she joined Prudential in Singapore, where she continued to make waves in the industry.

How has your leadership style evolved across the different companies you’ve worked with, and what have you learned as a result?

Having recently had more time to reflect as I transition from a CEO role to advisory, I’ve realised that a big part of my leadership journey has been about shifting from doing the work myself to needing to hire teams as my scope and responsibilities increased.

At some point in your career, you move away from being the one doing the work to focusing more on hiring, developing and leading teams, setting the vision, goals, planning and monitoring execution.

There are two main aspects. One is understanding the technical side, like P&Ls, but the other, more important part, is the leadership piece. I’m naturally more of a team person than an individual contributor, and working in a team has always come easily to me. I’ve also been fortunate to work in companies, like General Electric and Citibank, that put a strong emphasis on developing leadership skills.

Historically, Life insurers have been focused on how they give their agents and partners more products to sell – and not necessarily the customer needs.

Angela Hunter

When it comes to moving into different roles, especially across countries, I’ve become clearer about what I’m ultimately responsible for and what skills I need within my team. I try to assess whether those skills are already there, whether they can be developed, or if I need to bring in someone from outside.

I’ve always believed my role as a leader is about helping the team to succeed and to help removing obstacles getting in the way of delivery and achieving goals, as well as to help the team develop their careers. I’ve never been afraid to hire someone who’s better than me in a particular area. I’ve had a lot of opportunities where people trusted me with more responsibility, so I try to do the same with my team. While sometimes you do need to hire externally for certain capabilities, it’s great when your internal team members are eager to take on more and have the confidence to grow.

You achieved an impressive 56% growth over five years by targeting the millennial family segment. Can you walk us through the key strategies and innovations that drove this success?

Whenever I step into a new role, like when I joined the Thailand team, I will spend the first 60 to 90 days talking to all stakeholders before making any major decisions on strategy or personnel. This includes internal teams, senior leadership, agency partners, and external bank partners. I focus on understanding what’s working well, what could be improved, and identifying common themes across the feedback.

When I joined Chubb, after gathering insights, I worked with the senior leadership team to develop a five-year plan, focusing on why growth had slowed in the previous years and identifying gaps in the market. We brought in external consultants to benchmark Chubb’s competitive position and collaborated with our marketing, product, and channel teams to understand our strengths and weaknesses.

Historically, Life insurers have been focused on how they give their agents and partners more products to sell – and not necessarily the customer needs. This is starting to emerge in Asia recently as it becomes increasingly more competitive.

The 56% growth came from understanding Chubb’s competitive position, addressing product and service gaps, and providing our agency teams with the tools they needed to succeed in the market.

Angela Hunter

One key initiative in my Chubb role was leveraging existing customer research on health, which had already been conducted globally. We then targeted two segments: young millennials and family millennials. The latter was particularly aligned with our agency channel, making it easier to develop a new proposition. We partnered with a wellness app company to build a targeted proposition, combining health research insights with a wellness app and an approach to family health coverage to offer a fresh, compelling proposition for the agency team.

The strategy paid off. In the first quarter after launching the new product, we turned negative growth into a 30% increase. From there, we continued to refine our product suite, enhance technology and service support, and address other market gaps. Despite the challenges of COVID-19, we rolled out a digital tool for customer quotes and illustrations, launched a critical illness product, and implemented other digital initiatives over three years.

The 56% growth came from understanding Chubb’s competitive position, addressing product and service gaps, and providing our agency teams with the tools they needed to succeed in the market. In addition, we worked with our global team to launch a digital proposition to Young Millennials with our existing and new partners.

Given the diversity across the APAC region from emerging markets like Vietnam to more developed ones like Singapore and China how have you adapted your leadership approach to be effective across such varied environments?

I think the best way to describe my approach is rooted in my upbringing. I was the youngest of nine children, so I spent a lot of time observing the dynamics around me. This early experience helped me develop strong observational skills, which have been invaluable in my career, particularly when working in diverse cultural settings.

I’ve always been fascinated by travel – and it’s a passion that’s taken me from London to Germany, to Australia, New Zealand, Singapore, and six years ago, to Thailand. Each move presented its own cultural challenges. When I first moved to Australia in my early twenties, the culture was quite different from the UK, even though both are English-speaking. Singapore was more challenging, and Thailand even more so, but I relied on my ability to read body language and adapted my communication style because of that.

I’ve always had a knack for breaking down business problems and working with teams to tackle them effectively. I see my role as helping the team succeed by removing obstacles to success. I believe that demonstrating genuine care crosses all cultural boundaries. Whether in Singapore or Thailand, showing that you care about your team builds strong relationships, often feeling like family after a few years.

I believe in the servant leadership model and leading with kindness and authenticity. People can tell when you’re genuine, and they respond positively to it, regardless of language barriers. This approach has been a cornerstone of my leadership style across all the diverse markets I’ve worked in.

You’re a founding member of the Asia Business Women’s Leader Council and Financial Executive Women in Australia. What do you see as the biggest challenges and opportunities for women aspiring to leadership roles in the insurance industry? And to add context, how do you see these challenges across Asia compared to more developed regions, like the West?

I truly believe there’s never been a better time for women who aspire to leadership roles, especially in the insurance industry. If you look at the leadership teams in some companies, it’s true that they’ve been predominantly male-dominated, depending on the company. But there’s a lot of ongoing work to level the playing field. By that, I don’t necessarily mean having an equal number of men and women in leadership, but rather creating an environment where everyone has an equal opportunity to succeed, including attracting women to the industry.

There’s a growing awareness of issues like unconscious bias, which affects both men and women. It’s not just about men having biases against women—everyone has unconscious biases. There are also differences in how women and men operate in the workplace and how this is perceived differently which can sometimes inadvertently hinder women’s progress. Many companies are working on programs to raise awareness about these differences and how they can affect women’s advancement in their careers.

Companies are now recognising this and are actively working to encourage women to step up, even if they don’t feel 100% ready.

Angela Hunter

For example, it’s often said that women tend to be more critical of their own qualifications when considering a new role, whereas men are typically more confident about what they can bring to the table. Companies are now recognising this and are actively working to encourage women to step up, even if they don’t feel 100% ready. They’re identifying high-performing women and having those crucial conversations to ensure these women are considered for leadership roles, even if they haven’t put themselves forward.

In places like Singapore and Hong Kong, we’re seeing significant progress. While Australia and the UK might be ahead in mandating diversity on boards, Hong Kong and Singapore are catching up. The Hong Kong government, for instance, has started mandating diversity on boards, which is a positive step.

Addressing unconscious bias and recognising the different ways women and men might behave in the workplace are key areas where progress is being made. Many companies in banking and insurance are making serious efforts to level the playing field, and it’s encouraging to see that momentum continue.

Could you also share your approach to governance and strategic oversight? What advice would you give to women who are aiming for board positions?

There are a couple of angles to consider here. First, if you’re already part of an executive team, meaning you directly report to the CEO, you’ll likely have some exposure to boards. The first piece of advice I give to people considering this path is to enrol in a board training programme. Such programs help you understand the role of boards, how to interact with them, what their purpose is, and what they do.

For anyone aspiring to join a board, whether they envision a full board career or just want to gain some experience, my first piece of advice would be to try joining a not-for-profit board or to get involved in subcommittees within your organisation. This could be through your role in finance, compliance, or risk, where you might have the opportunity to participate in board-related activities. If that’s not an option, look for not-for-profit organisations and volunteer for their boards.

The first step is really about understanding the role of a board member, and attending a training program can provide you with invaluable insights. The programme I attended at Hong Kong University also covered topics like board succession planning—how boards make decisions about succession, how they collaborate with executive search firms to find new members, and what they look for in terms of complementary skills. I found that part particularly useful.

One key element is building a strong external network throughout your career and finding supporters and sponsors that understand and will promote your value.

What key strategies should the industry adopt to close the protection gap.

Over the last five years the number of people taking out insurance is not growing despite increased appetite for health and protection post Covid. It’s been quite challenging for most insurers post Covid, with increased running costs and increases in claims. Many insurers are targeting high net worth customers and offsetting increasing costs with increase in premiums which is understandable.

The purpose of insurance is getting lost and insurance is not increasing penetration particularly in the mass market segments that need protection the most. The historical meaning and purpose of insurance was to spread risks in the community so when things happen people can be protected. First and foremost, insurers must revisit their core purpose—spreading risk and providing financial security to communities (not only to high value customers). This foundational goal has always been at the heart of insurance, and it’s crucial to address this to reduce the protection gap in Asia.

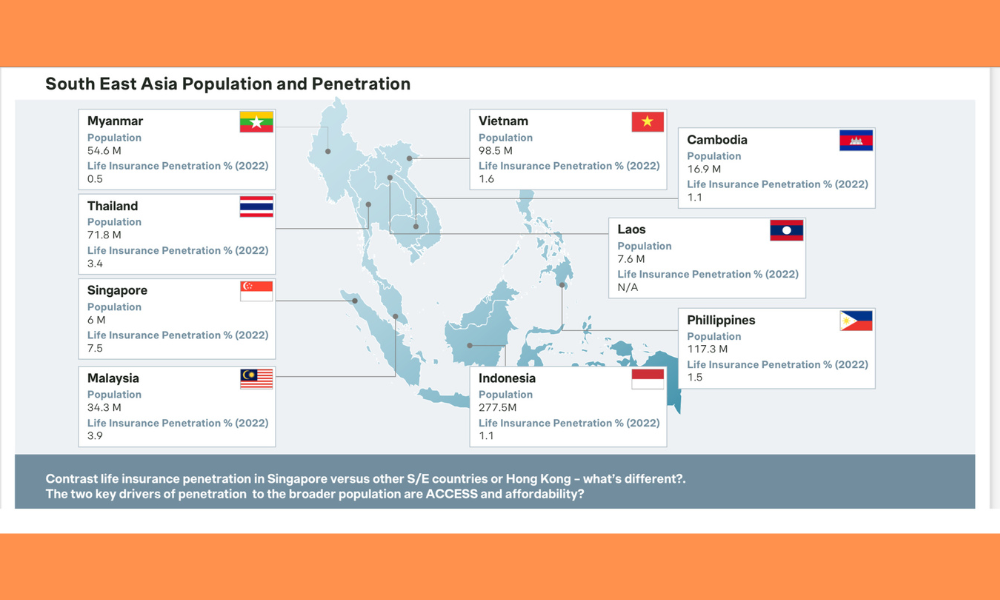

The COVID-19 pandemic highlighted these gaps, especially where financial stability was at risk and government support varied. For many regions, particularly in Asia, the insurance penetration remains incredibly low, often under 2%. This is a stark contrast to more developed markets like Singapore and Hong Kong, where penetration is much higher but mostly among the wealthy, and often focuses more on wealth accumulation rather than health and protection.

For many regions, particularly in Asia, the insurance penetration remains incredibly low, often under 2%. This is a stark contrast to more developed markets like Singapore and Hong Kong, where penetration is much higher but mostly among the wealthy, and often focuses more on wealth accumulation rather than health and protection.

Angela Hunter

To close this gap, insurers need to address the underserved segments (mass and lower mass market). They need to work much more closely with governments and regulators to improve financial literacy and make insurance more accessible. This means creating simpler products that are easier to understand and distribute through various channels, not just traditional agents and banks.

Insurers must adapt to the changing landscape by leveraging technology. Health insurance is very different to traditional Whole Life or annuity which are long term plans and not a regular claim product (usage) like health insurance. Insurers need to manage health portfolios very differently and need different skills sets, processes and technology to make their health portfolios more effective and their products more affordable, exploring innovations like digital microinsurance, and partnering with health tech companies to help with data analytics, claims and managing hospital networks. This approach could help reach underserved communities and manage costs better.

Insurers need to manage health portfolios very differently and need different skills sets, processes and technology to make their health portfolios more effective and their products more affordable, exploring innovations like digital microinsurance, and partnering with health tech companies to help with data analytics, claims and managing hospital networks. This approach could help reach underserved communities and manage costs better.

Angela Hunter

Lastly, there’s a need for insurers to address internal challenges, such as outdated legacy systems and increased claims costs post-pandemic. By investing in technology and process automation, insurers can improve efficiency and profitability.

In summary, to bridge the protection gap, the industry needs to ensure it’s strategies and plans to its purpose with modern needs, embrace technological advancements, and work collaboratively with regulators and partners to offer more accessible and relevant insurance solutions.

How do you see the role of insurance changing in the next few years, especially with issues like microinsurance, climate challenges, and rising prices?

Looking ahead, the role of insurance is definitely set to evolve in response to current challenges like climate issues, rising prices, and the growing interest in microinsurance. Insurers will need to adapt to these realities to stay relevant and profitable.

One major shift we’re seeing is an increased focus on health insurance. Many insurers have expanded into wellness offerings over the last 5-10 years and investments in digital health solutions, though not all of these initiatives have been as successful as hoped. For instance, most of the top Life companies invested in wellness apps however, they have been more of a marketing tool rather than fully integrating these into a cohesive and effective customer offering from pre-sale to claims and service and this remains a work in progress.

With rising costs and changing customer needs, some insurers are also exploring partnerships with fintech companies and health tech firms. This could involve offering microinsurance products or improving access to services like telemedicine. Such collaborations could help insurers reach new customer segments and manage costs more effectively.

Another key trend is the use of technology to streamline operations and reduce costs. Insurers are investing in AI and process automation to improve efficiency. While much of the tech focus in the past has been on sales and customer-facing tools, there’s a growing need to address internal processes and operational costs.

Overall, the insurance industry will need to continue evolving, embracing new technologies, and finding innovative ways to manage costs while meeting changing customer expectations.

With all these changes, the industry will need more talent. What advice would you give young women who want to lead in this field, and how should they prepare?

For young women aiming for leadership roles, here’s some advice based on my experience: First, get excited about the evolving nature of the insurance industry which may have been seen as more of an underwriting career. It’s becoming more customer-focused and tech-driven, which opens up plenty of opportunities. Don’t let traditional perceptions hold you back—there’s a lot of innovation and challenge here that’s really exciting.

Focus on developing a diverse skill set across different functions and develop leadership and strategic development. Diverse leadership experience across functions and locations will provide skills that are unlikely to be automated in the future. These roles require a mix of technical skills and people interaction, which is where you can really shine. Also, pay attention to how technology is reshaping the field. While some tasks might get automated, strategic and customer-centric roles will continue to be important.

In essence, embrace the industry’s changes, blend your technical skills with a strong emphasis on leadership and communications, and keep building a well-rounded skill set. This approach will help you stand out and succeed in the evolving landscape.

Interview by Joanna England