Emerging from the disruption of the pandemic, Accenture finds pressure on technical and market prices in many personal lines, as well as an increased focus from consumers on value for money and customer service.

Inevitably, insurers will have to further streamline their businesses to meet this new baseline on price and experience. However, beyond merely riding out what is in many respects a race-to-the-bottom, they must also back themselves to find – and exploit – new pockets of growth, many of which are themselves results of COVID-19.

The challenge will be to strike the right balance between these two things, meeting the “table stakes” whilst delivering on “wildcard” opportunities. Accenture explores both across today’s and next week’s post. First though, a quick review of what the pandemic has meant for consumers.

How has COVID-19 impacted consumer risk and appetite?

Government lockdowns, starting in March 2020, have led to widespread furloughs and home working in many sectors, with major knock-on effects for UK society and the economy. The high street has cratered, e-commerce is booming, and gardens are in demand. From an insurance perspective, the most striking consequence is how much fewer people are driving.

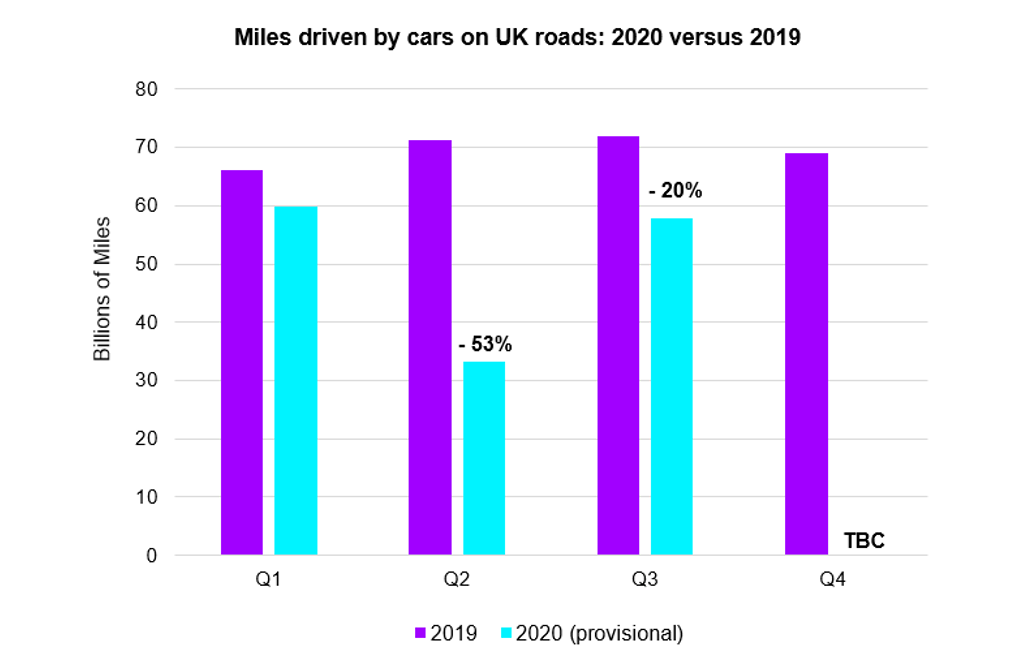

UK car traffic dropped 53 percent year on year in Q2 2020 and 20 percent in Q3, according to provisional estimates from the Department for Transport. And, even when restrictions are fully lifted, we can reasonably expect some lasting effect.

Less driving from consumers inevitably means less driving-related risk. How much and how quickly this will affect insurers’ new business (and overall top lines) is not yet clear, as plenty of other factors prop up the market. Car owners are legally obliged to have insurance, for instance, even if they’re not actually using their vehicles.

However, actuarial models that ignore reduced miles driven will not discover the true price floor – meaning that, for all that premiums may remain high, they will be on soft ground.

Many pandemic-related trends – such as remote working and reduced vehicle use – show no signs of reversing themselves, regardless of the vaccine rollout, so it looks like pricing pressure is here to stay, at least in the motor. Add to this an incipient recession, with all the curbs on consumer spending that brings, and Accenture can foresee an acceleration of the race-to-the-bottom in UK personal lines.

This is precisely why insurers must explore new growth prospects on the side, as a way to hedge against commoditization and margin compression. Fortuitously, just as the pandemic has dampened some traditional risk pools down, it has stoked others up. We will explore three such risk opportunities – home cyber risk, pay-as-you-drive solutions, and cover for alternative transportation – in our next post.

None of this must distract from the need, in the meantime, to meet evolving baselines for price and service; there is no point speculating on future growth if you fall behind in the main race. It is on this that we focus for the remainder of today’s post: how insurers can use digital technologies like automation and cloud to meet the table stakes of the new normal.

Table stakes 1: Value for money

Pricing pressure is nothing new in UK personal lines. So, in some sense, value for money has long been table stakes – although markets, especially on aggregator sites, have not always worked efficiently in this regard.

Dual-pricing allowed home and motor insurers to offer aggressive introductory discounts with heavily backloaded pricing, whereby policies representing poor value overall could appear to represent good value at the point of sale. This drove huge competition not just around actual value for money but also around the illusion of value.

However, this is set to change following recent reform from the FCA, as firms will now have to maintain parity between introductory prices and renewal prices. So, to advertise a lower price, insurers will have to make genuine reductions to the cost base and pass those savings on to customers – instead of funding lower prices via “loyalty taxes” and other sleights of hand.

While this move brings plenty of uncertainty and disruption, it also affords some much-needed clarity: with reduced scope for tactics, insurers can finally get strategic about pricing, by committing to big-name technologies with the potential to transform the cost base. Automation has a big role to play here. It’s also time for insurers to move beyond a toe-in-the-water approach to the cloud.

Table stakes 2: Customer service

It is not only on price that COVID-19 has raised the stakes in personal lines. The pandemic has also proven to be the big league for customer service.

Those firms that have prospered of late, none more so than Amazon, have done so thanks to early investments into digital – and have set consumer expectations for the years ahead. Things recently considered the leading edge of insurance customer experience are now the baseline. For a start, customers want insurance on their terms – 24/7 and on their preferred device – and will punish poor service by shopping elsewhere.

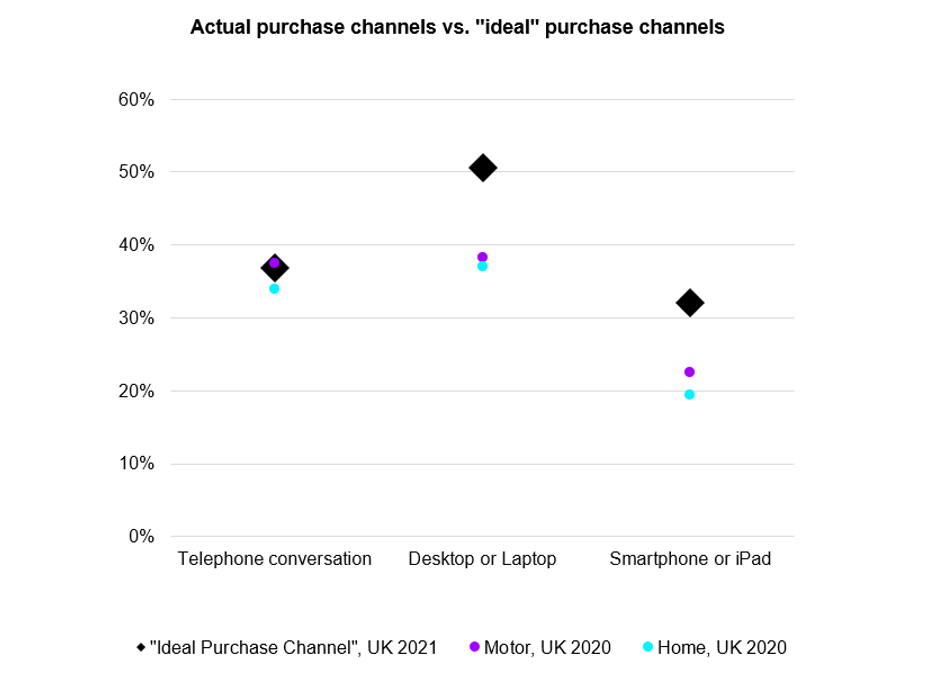

In Accenture’s Insurance Consumer Study 2021, they found high demand from UK consumers for desktop and mobile as part of their “ideal” channel mix for buying insurance – beating the actual distribution share for these two channels immediately before the coronavirus outbreak.

Put simply, this suggests there is unmet demand for digital channels in UK insurance. Carriers would therefore do well to bolster digital distribution (on their own platforms and on partners’) and expand customer self-service options like automated quoting and paperless claims. The easy scalability and rapid cycle time of cloud-based solutions are a trump card in all these cases.

At an operational level, cloud – and digital solutions more broadly – can help insurers avoid potentially damaging situations, like Accenture saw during the initial lockdown last March. Here, UK insurers witnessed a huge spike in customer calls, in some cases a 200 percent increase on March 2019 levels (according to the ABI), enough to leave many customers hanging.

To increase the resilience of their customer-service function, insurers can deploy smart tools like chatbots, rules-based triaging, and offline-to-online nudges, all of which reduce pressure on the core team. By placing the call center itself in the cloud, they gain more flexibility when it comes to scaling the team up or down at short notice, as well as an extra layer of business continuity.

Meeting these table stakes – value and service – will help insurers ride out the race to the bottom, but it won’t help them transcend it.

Source: Accenture