Prepared Minds involve our team honing in on specific categories and industries, being proactive, talking to our network, researching the trends shaping tomorrow’s world, finding the category leader – and then moving fast (for the right reasons!). Our Prepared Minds ensure that, by the time we invest, we share the same commitment and conviction as our entrepreneurs. This Prepared Mind series provides a snapshot of some of the areas our teams have been looking at and their predictions for how the landscapes will develop.

Mapping out the insurtech landscape

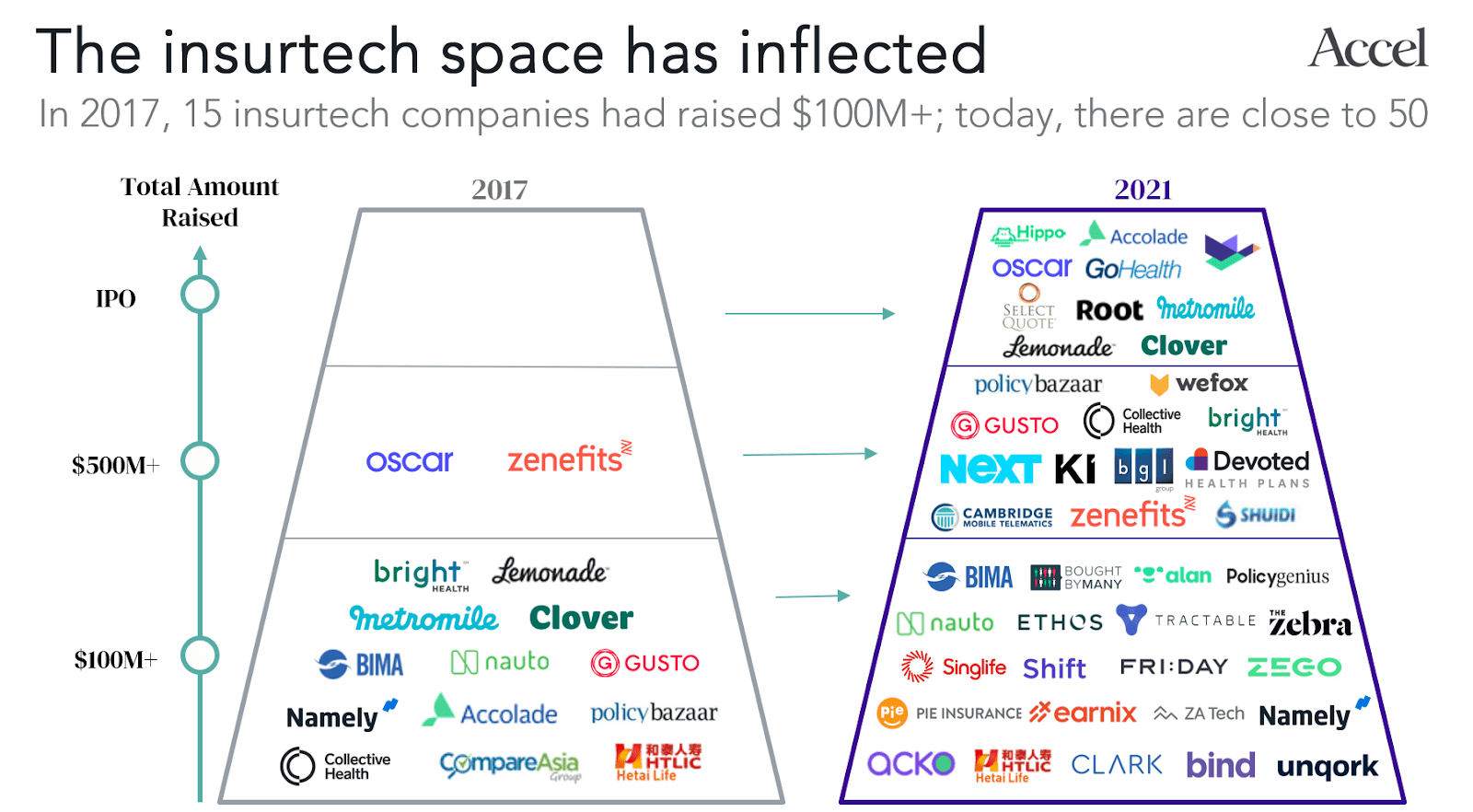

Insurtech is a huge, global $6 trillion industry. While it’s certainly been hotting up over the last year in particular, it remains an industry dominated by legacy practices that are ripe for change, and we’re still at the early stages of innovation. In fact, we believe we’ve only seen a fraction of what’s possible in this space. Since our last Insurtech Prepared Mind in 2017, there’s been massive growth in activity and annual insurtech funding has increased by more than 3x. The shift is particularly clear when comparing the number of insurtech companies which have raised more than $100M:

This rapid increase in activity has been driven by four key factors:

- Digital journeys: There’s been a shift in consumer and business expectations as both now look for engaging and entirely digital experiences, with instant pricing and rapid claims processing

- Product innovation: New data and distribution channels have emerged, employing innovative data sources and machine learning to better assess risk. Digitisation and APIs give rise to new embedded insertion points (e.g. e-commerce point of sale)

- Funding and exits: Multi-billion dollar IPOs in insurtech, led by Lemonade, have paved the way for more investor appetite and activity in the space

- Talent: Top calibre teams are emerging. World-class leaders are leaving incumbent insurers but also well-funded unicorns to start new companies and insurtech is seen as the next big fintech opportunity

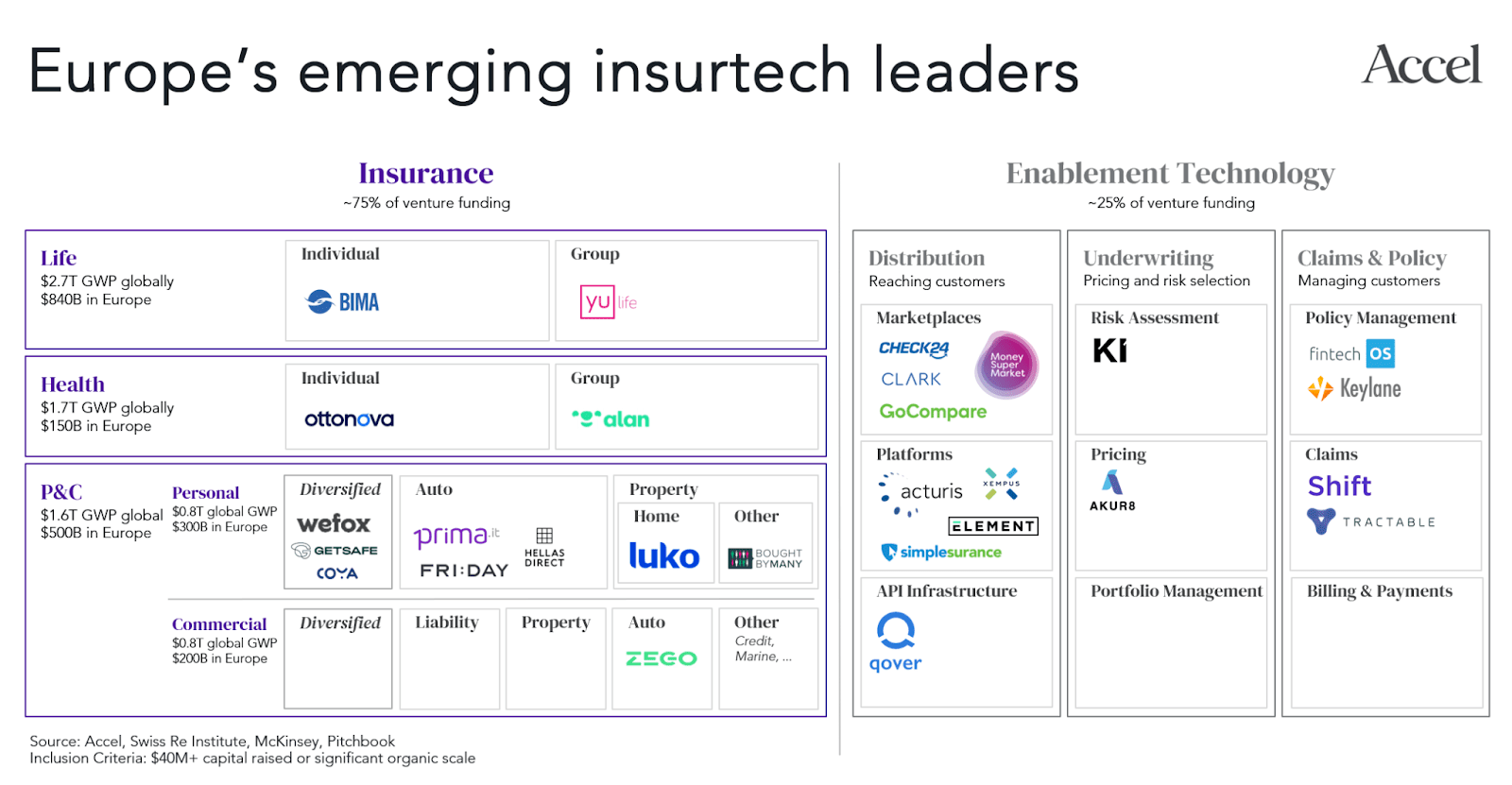

Europe in particular has seen a major inflection this year, with five new insurtech unicorns minted in the past four months – Alan, Bought By Many, Shift Technology, Tractable and Zego. We’ve also seen the largest ever round in an European insurtech company, with WeFox’s $650M Series C. At the current pace, 2021 is set to more than triple the largest ever funding year for European insurtech and exceed €4B in venture investment per dealroom.co analysis.

Mapping the leading European scaleups across different categories of insurtech shows both the exciting group of current companies, but also the huge white space opportunities that exist for new leaders to emerge. The total addressable market (TAM) in different insurance categories is staggering, with commercial insurance in Europe alone representing approximately $200B* of gross premium.

Predictions for the future

Here are our five predictions for what’s in store for insurtech:

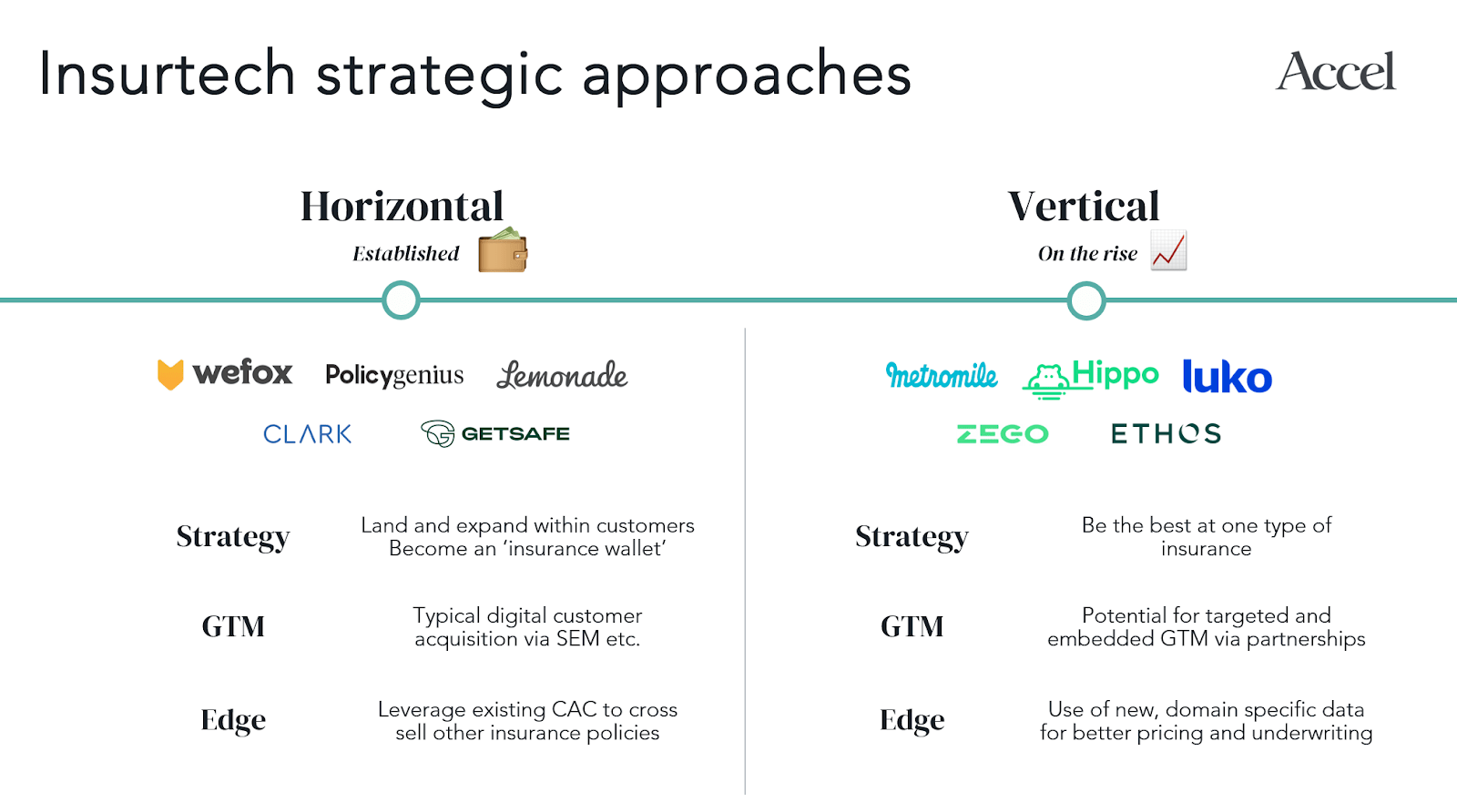

1) Verticalization of insurtech

With consumer expectations and needs shifting, we’re starting to see the fragmentation and verticalization of insurance. A new generation of insurtech companies have seen the potential to bring new data sets and targeted GTM models together to create a far superior product in their space compared to legacy, generalist incumbents. Similar to the unbundling of core banking we’ve seen in fintech offerings (lending, FX, payments etc.), we expect the insurance industry to follow the same trend in both B2C and B2B. We’re excited to be working with early leaders here including Ethos, bringing a step change to the US life insurance vertical by employing 300,000+ data points in determining their policies, and Luko, combining fully-digital European home insurance with more holistic home care services. Over time, some of these vertical winners will naturally move horizontally (as Lemonade has been doing) to expand their TAM, but we believe that vertical specialism will become the dominant initial approach for new managing general agents (MGAs) and full-stack carriers.

2) The rise of SMB insurance across Europe

Just as small and medium businesses (SMBs) have traditionally been overlooked by software providers, they’ve long been underserved by legacy insurers. The widespread business disruption caused by the pandemic has forced SMBs to reconsider their insurance arrangements and the resulting market opportunity is huge, with SMBs representing over 50% of Europe’s GDP and 99% of all businesses. The way SMBs want to purchase insurance is changing along with demographics and we see today’s younger business owners far more comfortable buying online as they do for their personal insurance. In addition, the use of new data sources is unlocking the potential for unprecedented insurance cover which reflects the reality of a business’s current size and activities, rather than relying on stale questionnaires. With Next Insurance, Embroker and others making waves in the US SMB space, we feel a similar approach will soon take off in Europe.

3) Embedded insurance everywhere

Connecting customers with insurance products through channels and brands they already trust can unlock massive opportunities on every side of the transaction. We see embedded insurance distribution correcting one of the markets’ worst inefficiencies: the insurance purchase is typically disjointed from the purchase of the item to be insured. For insurers, embedded models can lead to more data (better loss ratio) and efficient distribution (better expense ratio); for consumers, more relevant cover and a better customer journey; for brands, better monetization of their community. For example, Tesla is able to offer up to 30% cheaper auto insurance rates to its vehicle owners because it has so much data which can be used for more efficient pricing and underwriting decisions. Our portfolio company Acko is bringing embedded models to bear across mobility, health and other insurance lines in India with partners including Amazon, Ola and OYO. Ultimately, we think embedded insurance will make a dent on every insurance line in the coming years.

4) Insurtech goes further down the stack

While most insurtech momentum to date has come from players innovating on distribution and the customer experience, we believe another wave of landmark companies is still to come from deeper in the tech stack. The core systems used by the majority of insurers still sit on mainframe, but the shift to cloud native software we’re already seeing in banking is starting to come to insurance. COVID-19 has been a catalyst for digital transformation with 88% of insurers stating that legacy systems prevent them from transforming fast enough. In parallel, newer MGAs have been building and maintaining their own tech stack, which is inefficient when compared to a third party platform provider. Analogous to the rise of Banking-as-a-Service platforms like Mambu, Swan and Unit, there’s now an opportunity for API platforms in insurance which cater to the needs of MGAs, incumbent carriers and brands, and intrinsically improve the operations and cost structure of the entire industry.

5) Europe to see its first $B+ insurtech exit in 2022

Lemonade, Oscar, Hippo, Assurance, Clover, Metromile, Root and others have shown the world what’s possible in terms of multi-billion dollar exits in insurtech, be it through IPO, SPAC or M&A. However, blockbuster European outcomes have been conspicuous in their absence to date when compared to the US and Israel. With a growing stable of unicorns and ‘soonicorns’ (including Acturis, CLARK, Luko and YuLife) we expect to see the European ecosystem yielding its first landmark exit in the next 18 months. As we have witnessed elsewhere, major exits tend to lead to a flywheel of more outstanding founders, advisors and companies – and we couldn’t be more excited about the future.

Source: Accel