When we meet up with Anthony Peake in a hotel lobby in Barcelona, he’s more excited to talk about his recent dragon boat races in Serbia than discussing his latest foray into Insurtech AI solutions.

But Peake is a man who has been in the business of technology for several decades, and he has a level of enthusiasm for life and ideas that is hard to match. Indeed, he led the marketing team for Apple when they launched the Mackintosh in the UK in 1984 and, since then, he’s had leading roles in the industry with companies such as Oracle, British Telecom, and General Electric.

He also launched Intelligent AI in April 2020, just as the world was heading into lockdown and access to clients and investors was difficult. Unperturbed, and with the kind of enthusiasm that wins dragon boat races, he self-funded the start-up, which has since won the Zurich UK Innovation Championship, beating 400 other InsurTech companies in the process. It then went on to win the QBE Global Innovation Challenge, as well as gaining substantial innovation grants and contracts from Innovate UK and the European Space Agency.

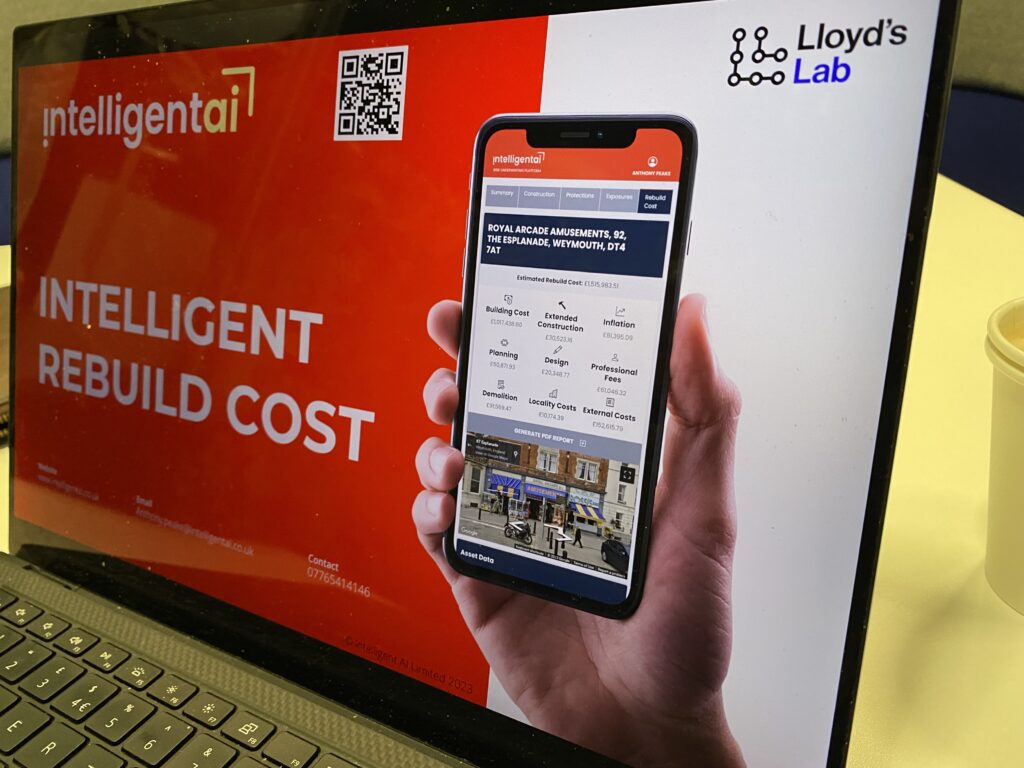

Intelligent AI has also just announced the launch of its ground-breaking Intelligent Rebuild Cost Validation Platform, to coincide with graduating from Lloyd’s Lab, Cohort 10, which is designed to address the long-standing challenge of underinsurance in the commercial property market.

Can you tell us about your early interest in technology? Was it always a passion?

I studied electronics and computing during my university days. However, back then we were working with older technologies like the Apple II, Hex, and BASIC programming. It was a different era of computing compared to today. When I finished college, I went to a jobcentre in Liverpool and there were two job cards available.

One was for welding and the other was for launching a new computer for a software company. Since the interview for the computer company was scheduled for four weeks later, I decided to take both cards. I ended up spending three weeks doing welding before the job interview, which turned out to be for Apple. They were about to launch a new computer called the Macintosh and needed someone to lead the launch.

Could you share more about your experience with Apple and the early days of digitisation?

Working at Apple was an incredible experience. At that time, IBM was the dominant force in the technology industry and Apple stood out by being different. The company introduced a whole new world of graphical interfaces, icons, and cut-and-paste functionality. It was a departure from the text-based green screens that were prevalent. Apple’s brand identity revolved around being distinct from the rest. For me personally, it was an exciting journey, starting in Liverpool and eventually spending a significant amount of time in Cupertino, California.

The culture at Apple was truly unique. The company embraced a philosophy of being distinct and non-conformist. It aimed to challenge the status quo and provide users with a different experience. Transitioning from the traditional green screens to the world of icons, design, and ease-of-use was revolutionary. Apple’s focus on design and attention to detail permeated the entire brand. As a young graduate, it was a refreshing and rewarding environment to be a part of.

Your career seems to have been centred around digital transformation. Can you elaborate on that?

Absolutely. Throughout my career, I’ve been involved in various aspects of digital transformation. Starting with early endeavours in typeface design and desktop publishing, I have always been drawn to the meticulous details of design. My passion for pixel-perfect precision and harmonious colours has been a constant throughout. Interestingly, many of the projects I have undertaken have been commended not only for their functionality but also for their beauty. Clients have often commented on the aesthetic appeal of the solutions we’ve delivered.

Can you provide an example of a project that showcased this attention to detail and design?

Certainly. One project that comes to mind is the one we undertook for XL Catlin, a few years ago. Before the project began, a senior stakeholder emphasised the importance of it being beautiful. In my final presentation during the tender process, I showcased every mock-up design screenshot on Apple devices—an Apple laptop, an Apple screen, and an iPad. It was a testament to the meticulous focus on aesthetics and the belief that design should be an integral part of any functional solution. The client approved.

It seems like you have a deep understanding of both technology and the importance of people in the industry. Can you expand on that?

Absolutely. Technology is only half of the equation; the other half is people. No matter how advanced or cutting-edge the technology may be, its success ultimately depends on its usability and how it resonates with users. It’s easy for us to get caught up in the technical aspects and forget about the human element. I often find myself challenging my own thinking and striving to strike a balance between technological innovation and user-centric design. Taking people along on the journey is crucial to achieving successful outcomes.

How did you transition from the technology industry to the insurance industry?

It all started eight years ago, when I joined a struggling bespoke software development company. Although the company catered to various industries, it had a few insurance clients among its customer base. Recognising the potential for innovation and growth in the insurance sector, I decided to focus my efforts on transforming the company’s approach to serving insurers.

By shifting the team’s focus from supporting old legacy systems to working on more innovative projects, we were able to tap into the industry’s potential. Moreover, my experience in change management and dealing with large organisations undergoing transformation allowed me to navigate the complexities of the insurance landscape effectively.

How did you manage to secure funding and investments for Intelligent AI?

Despite the challenges posed by the pandemic, we were able to secure a £350,000 grant from Innovate UK, followed by another £100,000 grant. Additionally, we raised £400,000 through a pre-seed round of funding in April 2021. Since then, we have successfully attracted around £2 million in investment and secured approximately £1 million in grants. These funds have been crucial in supporting the development of our platform and driving our long-term vision forward.

Can you share more about your participation in the Lloyd’s Lab cohort and how it has contributed to your vision for Intelligent AI?

Joining the Lloyd’s Lab cohort was a strategic decision aligned with our vision of becoming a global organisation. The goal was to build a platform and establish strong data foundations in the UK and the US, paving the way for global partnerships.

These partnerships will be instrumental in expanding our presence into the US and Asian markets. However, before going global, it’s essential to establish a strong foothold across Europe. Participating in the Lloyd’s Lab allowed us to nurture relationships and explore opportunities within the European insurance landscape. This was our second time in the lab, as we were previously part of a group focused on insurance risks, supply chain risks, and audit risks. We recognised the potential for aligning data across these domains and sought to leverage that alignment in our platform.

The support of Lloyd’s Lab and the fantastic insurance mentors that give up their time to support lab cohorts and introduce them to their businesses to open up commercial opportunities has been invaluable.

What specific challenges does Intelligent AI address in the insurance industry?

One of the key challenges we address is the issue of underinsurance in commercial properties. Our platform, particularly our verticalised solution for rebuilding costs, tackles this problem head-on. Currently, an alarming 79% of commercial properties in the UK, and likely globally, are underinsured by at least 30% and often more than 50%. This stems from the high costs associated with getting accurate reinstatement valuations for buildings. Owners often resort to estimating values or using outdated data, leading to substantial gaps in coverage.

Through our intelligent risk underwriting platform, we have collected extensive data on building locations, materials, heights, shapes, and occupancies. Additionally, we have incorporated the costs of materials, supply chains, and labour. By leveraging this data, we can accurately determine rebuilding costs in seconds, compared to the hours it typically takes for manual evaluations. This empowers clients to ensure their entire property portfolios are adequately insured, while insurers gain better visibility into the true values at risk.

How does underinsurance impact both insurers and clients?

Underinsurance poses significant risks for both insurers and clients. Insurers face exposure to potential losses when properties are undervalued and the coverage is insufficient. They may find themselves inadequately prepared to handle claims in the event of disasters or accidents. On the other hand, clients face financial risks when their properties are undervalued. If a client suffers a loss and their insurance coverage falls short due to underinsurance, they may not receive adequate compensation for the damages.

This issue has become more critical in recent times, with the insurance market transitioning from a soft market to a hard market. Insurers now require more accurate data and profitability due to various factors, including the COVID-19 pandemic and the high-profile business interruption cases. Our platform addresses this challenge by providing insurers and clients with precise rebuilding cost valuations, reducing the risks associated with underinsurance, whether you are looking at a property or a portfolio of millions of properties.

Our future expansion plans involve securing a Series A round of funding in Q2 of next year. This investment will enable us to expand our presence across Europe, US, and into Asia. We already have a strong foothold in the UK and the US, and our goal is to establish a global platform through partnerships. By targeting key European markets like Germany, Italy, Spain, and beyond, we aim to become a truly global InsurTech platform. Our focus on verticalised solutions, such as our rebuilding cost assessment and Carbon Calculation, will continue to drive our growth and provide valuable services to clients and insurers worldwide.

Can you explain the approach of Intelligent AI towards AI and its focus on auditability and ethics?

Intelligent AI takes a distinct approach to AI by prioritising auditability and ethics in its operations. Rather than relying on black box machine learning (ML) algorithms that analyse large amounts of unstructured data and providing insight that can’t be fully checked, Intelligent AI has built its platform from the ground up using AI algorithms.

The platform focuses on structured data, particularly tables, tabular data, and whole sentences found in risk reports, which comprise approximately 70% of the content. By training the model with a template of risk reports and identifying specific types of data within those reports, Intelligent AI ensures transparency and understanding of how the system arrives at its conclusions. This approach allows for full auditability, enabling users to trace back the data sources and understand the decision-making process.

Intelligent AI also acknowledges the presence of biases in data and emphasises the need to address them. The company recognises that data can be biased, and understanding and accounting for biases are crucial for ethical AI implementation. They emphasise the importance of regulatory compliance and ethical considerations in building and deploying AI systems.

How does Intelligent AI leverage AI to identify growing risks and enhance risk management?

Intelligent AI uses AI algorithms to analyse open data, satellite data, and proprietary data sources to identify and evaluate growing risks before they materialise. By leveraging these diverse data sets around construction, occupancy, protections, and environmental, the company aims to provide insurers with proactive risk assessments and enable them to take timely actions to mitigate potential risks. For example, by analysing data related to previous incidents and risk factors, such as fire callouts and building refurbishments, Intelligent AI can identify patterns and trends that suggest increasing risks.

This approach allows insurers to intervene and address risks proactively rather than reactively, potentially preventing or minimising losses.

The company’s focus on analysing data and providing valuable insights to insurers aligns with their objective of optimising the time spent on administrative tasks. By automating data analysis and risk assessments, Intelligent AI enables risk engineers and underwriters to dedicate more time to engaging with clients, educating them about risks, and offering tailored risk management solutions to prevent and mitigate risks.

What is your long-term vision for Intelligent AI?

We have started by automating complex risk models for commercial property for insurers, brokers, and property owners. We have built on that ‘Digital Twins of Risk’ innovation, and have just launched a new platform that automates the rebuild cost calculations for millions of global businesses, taking a traditional manual process that takes 60-90 minutes per building down to less than 10 seconds, whilst improving accuracy and lowering cost, and are moving into valuing buildings globally from space with a project that is co-funded by the European Space Agency. Our next focus is likely to be on automating carbon footprint benchmarking calculations, to help drive sustainability and NetZero.

What’s new on the horizon for Intelligent AI?

The company’s commitment to auditability, ethics, and addressing biases aligns with their purpose of providing accurate risk assessments and early identification of growing risks. They aim to empower insurers to have a deeper understanding of their portfolios and clients’ risks while optimising the time spent by risk engineers and underwriters on value-added tasks.

Intelligent AI recently launched our Intelligent Rebuild Cost Platform for Lloyd’s of London. The platform addresses the significant challenge of underinsurance in commercial properties by providing accurate rebuilding cost valuations. Through mentoring and collaboration with major insurers in the Lloyd’s Lab, Intelligent AI has gained valuable insights and enhanced the quality and auditability of its models. They are currently running large-scale pilots with prominent organisations to validate the platform’s effectiveness.

In addition to addressing underinsurance, Intelligent AI is expanding its model beyond risk assessment and valuation. We are incorporating environmental, social, and governance (ESG) considerations into our platform, enabling the calculation of the carbon footprint and sustainability of buildings. By quantifying the impact of sustainability on asset values and other factors, Intelligent AI aims to encourage greater sustainability practices and inform investment decisions.

What inspires you and the Insurtech industry today?

The slow transformation of insurers inspires me because it demonstrates their recognition of the need for change and the potential for transformation within the industry. While insurers may be slow to adopt new technologies and approaches, the fact that they understand the necessity of transformation is encouraging. Meeting individuals who share the vision and enthusiasm for change, such as those encountered at conferences and events like Lloyd’s Lab, further reinforces the inspiration to drive innovation in the industry.

Additionally, the presence of numerous start-ups and innovators within the InsurTech space is inspiring. These entities are developing various components and ideas that collectively have the potential to revolutionise the entire insurance industry. Whether it’s in hyperlocal flooding, Internet of Things (IoT), satellite technology, or other areas, there are many individuals and organisations building the necessary foundation for transformative change.

However, there is also a recognition that the insurance industry still has progress to make in terms of embracing innovation and agility. The bureaucracy and due diligence processes can be cumbersome and slow-moving, which can be a challenge for InsurTech companies striving to bring innovative solutions to market quickly.

Nevertheless, despite these challenges, the overall readiness of the insurance industry to undergo transformation and the presence of brilliant ideas among InsurTech start-ups continue to inspire and fuel optimism for the future.

Interview by Joanna England

Joanna England is an award-winning journalist and the Editor-in-Chief for Insurtech Insights. She has worked for 25 years in both the consumer and business space, and also spent 15 years in the Middle East, on national newspapers as well as leading events and lifestyle publications. Prior to Insurtech Insights, Joanna was the Editor-in-Chief for Fintech Magazine and Insurtech Digital. She was also listed by MPVR as one of the Top 30 journalist in Fintech and Insurtech in 2023.