Via Silvia Milian, Accenture

The insurance outlook for Europe

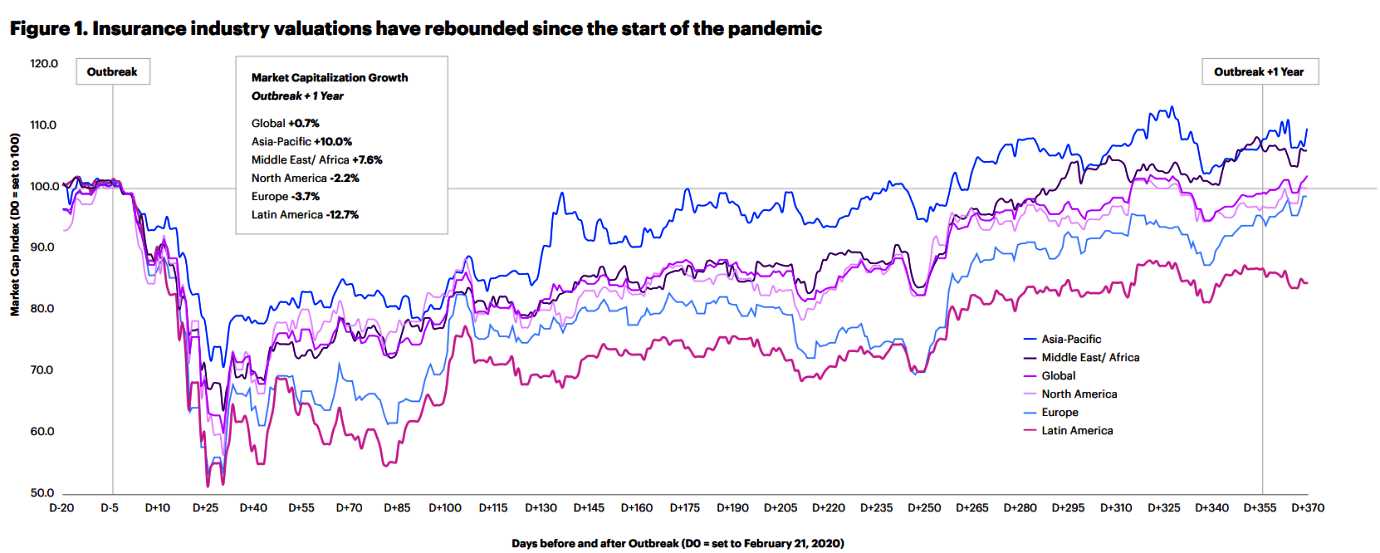

Despite a challenging year of recessionary conditions and disrupted risk models, Accenture’s analyses predict significant growth for the insurance market over the next five years. Within that growth, we foresee a shift in revenue pools. As we can see in the figure below, the global economy is showing signs of strengthening after the pandemic, and the insurance industry is proving its resilience.

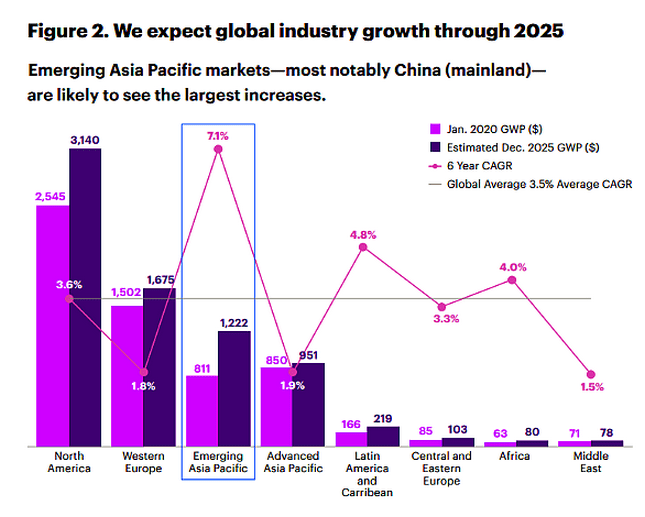

A good gauge of the projected activity in the insurance industry is to look at the anticipated GDP. Insurance is directly linked to increased asset ownership and use. For this reason, Accenture’s projection of $1.4 trillion in global industry growth is consistent with forecasted increases in global GDP. However, as shown in the figure below, Emerging Asia Pacific Markets are expected to see the highest growth (of 7.1 percent), with Western Europe’s projected growth at 1.8 percent. There is no doubt about it, industry growth is a priority, and the best way to drive that growth is through innovation.

To ensure long-term profitability, insurers need a new strategy. They can no longer rely on familiar products, channels and historic retention rates in the fast-changing context of rising costs, volatile markets, and increasing consumer demand for digital services. Accenture predicts that almost half a trillion dollars ($480 billion) of the $7.5 trillion in GWP expected in five years, or approximately 7 percent, would be heavily impacted by innovation.

It’s time to innovate for growth 15 percent($200 billion) of the projected $1.4 trillion industry growth would come from new risks, products and services. This would include new product innovation ($160 billion) and the monetization of value-added services ($40 billion). If insurers want to stand a chance in competing for this innovation-fuelled income, they need to create new products, services and revenue streams that both grow and retain their customer base.

Innovate for growth

Consider the case of Verti, an auto insurance company creating products that directly respond to what customers are looking for. After analyzing the data they collected, Verti discovered that users are highly incentivized by discounts on their insurance rates. This led them to launch the Verti Driver app, which uses phone sensors and GPS to determine how accurately the driver is following the rules of the road given the location they are in. Based on the data collected, Verti Driver generates a score, which makes certain discounts available to the driver, depending on their performance. Insurers can also respond proactively to the unique risks associated with the present-day environment. Beazley insurance, for example, has introduced a contingency policy that offers compensation for live virtual events that are canceled or disrupted owing to a transmission failure. Covering everything from large conferences, exhibitions, theatrical shows, concerts and sporting events this virtual event insurance is extremely relevant in the context of the pandemic. And although streaming live events is not new in itself, social distancing rules have caused many major events to either be cancelled, postponed or moved online. The policy covers first-party losses including organisational costs, expenses, or gross revenue from advertising and ticket sales.

Innovate for retention

Insurers can’t assume that they will retain their clients, or expect historic retention rates to continue. Although current insurance retention rates are at 85 percent for most insurers, we are already seeing signs that personal lines retention rates are slipping. Accenture’s most recent consumer study notes that US$2.0b of current revenues in traditional insurance distribution in Spain could be displaced by insurers offering digital distribution experiences, as customers purchase insurance on digital channels and third-party platforms. In addition to this, we expect that almost 5 percent of global premiums—approximately $280 billion—will be impacted by innovations in products ($140 billion) and shifts towards digital third-party platforms ($140 billion). With this kind of shift, insurers could see retention rates drop if they neglect to defend existing revenues through product and distribution innovation. Thankfully, many European insurers are responding to the call to innovate their client retention strategy.

Generali, for example, has created a digital, multichannel, and personalized experience to drive renewals. The engaging, tailored experience is delivered across multiple channels. Then, when it comes to the time for renewal, a custom email is sent to each client explaining their policy and coverage. At the end of the video, the agent calls the client to receive renewal approval and the updated policy is emailed to the client.

Pega has launched its Customer Service and Customer Decision Hub are tools to help insurers proactively offer retention actions before an unsubscribe request is generated. Pega continually adapts retention strategies and customer engagement to support customer needs and promptly shows empathy in every customer interaction. This is offered through an omnichannel tool, which allows to create end-to-end customer journeys, and deploy them in the different channels, so that they are available in the customer’s preferred channel.

As you can see above, leading insurers are using innovation to drive growth and create new revenue opportunities.

Source: Accenture